Mortgage Blog

Mortgage It Right!

Time to Check-In with your Mortgage!

January 13, 2021 | Posted by: Kelleway Mortgage Architects

There has never been a better time for your annual mortgage health check-up! By organizing a quick mortgage review each year, it may yield you some fruitful financial savings.

Your home loan review this year will examine the most common potential monthly savings opportunities, including high-interest credit card debt or fixed loan payments. Reviewing your mortgage terms and options annually could result in having more money left over at the end of each month - and who doesn’t want that?!

For instance, are you exercising your penalty free extra payment privileges? Do you have any? Prepayment privileges allow you the opportunity to pay up to 20% extra per month and a total of up to 20% lump sum per year - without penalty! This means that for a $300,000 mortgage on a 25-year amortization, a 20% monthly payment increase can generate $18,000 worth of savings AND help you to pay off your mortgage 5 years earlier! When you add-on the annual lump sum of $2,500, the savings are increased to just over $25,000 for the year and bumps you up to being mortgage-free 8 years earlier! You can also use the My Mortgage Planner app to calculate the potential savings from an extra payment.

When it comes to mortgage payments, another great question for your annual check-up is whether or not you are on the best payment frequency for your cash flow and to best optimize savings! Most lenders offer various payment frequency and an annual mortgage review can help identify the best frequency based on changing needs and cash flow situations. A monthly payment is simply a single large payment, paid once per month; this is the default that sets your amortization. A 25-year mortgage, paid monthly, will take 25 years to pay off but includes the added burden of one larger payment coming from one employment pay period. Alternatively, an accelerated bi-weekly payment pays your mortgage every two weeks. This frequency allows the mortgage payment to be split up into smaller payments vs a single, larger payment per month. This is especially ideal for households who get paid every two weeks as the reduction in cash flow is more on track with incoming income.

These accelerated bi-weekly payments also offer interest savings, as you are actually making an extra payment each calendar year. For instance, a $300,000 mortgage on an accelerated bi-weekly payment schedule will pay off your mortgage two and a half years faster and generate approx. $8,000 in savings! That's like getting a $10,000 a year raise just by changing your payment frequency!

Another area to look at during your mortgage check-up are your penalties. Breaking your mortgage term early, and before the scheduled contract maturity date, will almost always incur a penalty. The amount depends on various factors such as how far you are into the existing term, your current interest and rate type, your existing lender, etc. However, with today's rates sitting at such a historical low, there can still be savings! Now, if you break your mortgage early and incur a penalty, you can still come out ahead. For instance, it is possible to save $20,000 with a new low rate and incur a $15,000 penalty, which still puts you $5,000 ahead! Having an annual mortgage review can look at these options and determine if it is a benefit for you to chase these historically low rates.

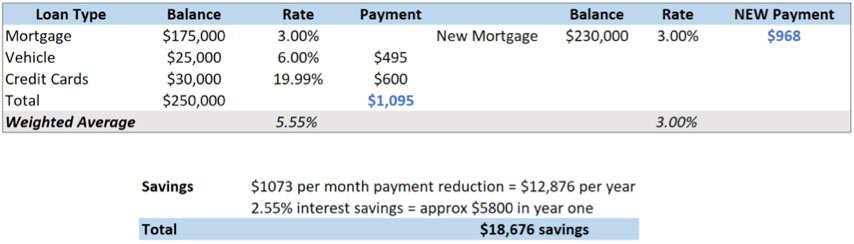

Beyond your current payments and interest rate, consumer debt outside of the mortgage is another important area for review. Did you know? The average Canadian has $30,000 of credit card debt, at approximately 20% interest?! Reviewing your home equity situation could yield $10,000 savings, per year, by rolling debts into your home equity loan. Contact me today to discuss this further and see if it is an option for you!

Please note this is just an example and your actual mortgage finances may be different.

Pay more to save more, pursue lower rates even with a penalty, and debt consolidation are just three examples of the financial savings an annual mortgage check-up with your mortgage professional can do! With interest rates at historic lows, now is the time to investigate all your options and perhaps save yourself thousands of dollars per year, especially if your current interest rate is over 3%! Imagine what you could do with the savings – anything from renovating or investing to going on a much-needed vacation or putting money towards your children's education.

Completing a straightforward annual review will keep your home financing as lean and trim as possible. In other words, you will have a clean bill of mortgage health, which is just what the doctor ordered! Contact me to set up a mortgage check-up today!

Email KMA

Blog Categories

- Main Blog Page

- Alt-A Lending Options (1)

- Announcements (18)

- Builder's Lien Removal (1)

- Community Relations (1)

- COVID-19 and Mortgage Deferral (8)

- Credit & Debt (15)

- Down Payment (2)

- Education and Courses (4)

- Financial Intelligence (17)

- Foreclosures (1)

- Fun Tips (52)

- Home Improvement (2)

- Legal Considerations (2)

- Line of Credit (LOC) (1)

- Mortgage Lenders (2)

- Mortgage Renewals (10)

- Mortgage Trends & Rates (14)

- Mortgage Types (13)

- Moving to Next Home (8)

- My Mortgage Planner App (5)

- Price per Square Foot (1)

- Prize Draw (41)

- Property Types (11)

- Purchase + Improvement (9)

- Qualifying for a Mortgage (14)

- Real Estate Contracts (2)

- Real Estate Market (12)

- Real Estate Taxes (7)

- Recipes & Serena's Tasty Tidbits (5)

- Relocation into Canada (1)

- Selling Your Home (3)

Blog Archives

- July 2022 (1)

- May 2022 (5)

- April 2022 (5)

- March 2022 (5)

- February 2022 (4)

- January 2022 (6)

- December 2021 (5)

- November 2021 (5)

- October 2021 (4)

- September 2021 (4)

- July 2021 (6)

- June 2021 (7)

- May 2021 (4)

- April 2021 (4)

- March 2021 (5)

- February 2021 (4)

- January 2021 (5)

- December 2020 (6)

- November 2020 (4)

- October 2020 (5)

- September 2020 (3)

- August 2020 (2)

- July 2020 (3)

- June 2020 (5)

- May 2020 (3)

- April 2020 (6)

- March 2020 (10)

- February 2020 (5)

- January 2020 (8)

- December 2019 (4)

- November 2019 (6)

- October 2019 (6)

- September 2019 (3)

- August 2019 (4)

- July 2019 (5)

- June 2019 (3)

- May 2019 (5)

- April 2019 (5)

- March 2019 (5)

- February 2019 (8)

- January 2019 (8)

- December 2018 (4)

- November 2018 (7)

- October 2018 (7)

- September 2018 (5)

- August 2018 (5)

- July 2018 (6)

- June 2018 (3)

- May 2018 (4)

- April 2018 (1)

- December 2017 (1)

- February 2017 (2)

- October 2016 (4)

- September 2016 (1)

- August 2016 (6)

- June 2016 (5)

- April 2016 (1)

- March 2016 (4)

- December 2015 (2)

- November 2015 (1)

- June 2015 (5)

- April 2015 (4)

- January 2015 (1)

- December 2014 (1)

- October 2014 (2)

- July 2014 (4)

- April 2014 (1)

- October 2011 (1)